Bank of England widely expected to hold 4% rate as inflation stays above target

Analysts anticipate no change at Thursday's rate decision, with inflation still running above target and food-price pressures easing only slowly.

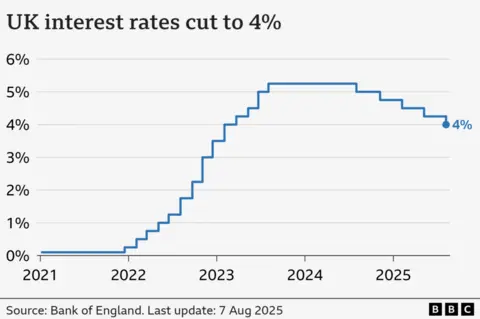

The Bank of England is widely expected to hold the Bank Rate at 4% when the Monetary Policy Committee announces its decision on Thursday at 12:00 BST, with inflation still running above the 2% target.

At its August meeting the MPC cut the rate from 4.25% to 4%, its lowest level in more than two years. Official data released this week showed inflation at 3.8% in August, driven by higher food prices, underscoring why policymakers are reluctant to ease policy further. Analysts say the balance of risks remains tilted toward keeping policy tight for now.

Last August, the decision to cut was described by Bank of England governor Andrew Bailey as finely balanced after a historic split vote among the nine MPC members. Thursday's vote is expected to be a straightforward hold, with no change anticipated, reflecting inflation still above target. If inflation moves closer to the target in coming months, a further easing could be possible later in the year, though the path remains uncertain.

The Bank Rate shapes the pricing of loans and savings, and lenders use the rate as a benchmark for new mortgage offers. Mortgage rates have edged down slightly since August, but further moves are uncertain. Analyst Rachel Springall of Moneyfacts said savers have seen returns fall and should consider switching to higher-yield accounts.

Global context shows policy divergence and growth concerns. The government would like to see rates fall further to boost growth, but inflation risks remain. In the United States, the Federal Reserve cut rates to a range of 4% to 4.25% for the first time since December, while the European Central Bank held rates at 2%.

Markets will weigh the decision against data on inflation and the Budget due later this year. The central bank's stance suggests rates may stay on hold through the autumn, with the possibility of cuts if inflation cools.

For households, the outcome matters for mortgage commitments and savings returns, and the direction of rates remains a key driver of consumer finance costs.