Four Big Worries Loom as Markets Hit All-Time Highs

As stocks reach record levels, investors weigh rate-cut drama, reshoring bets, jobs-data reliability, and Social Security funding in a shifting economic landscape.

Stocks at or near all-time highs abroad and at home have done little to quiet a growing sense of nervousness among investors, a sentiment that Ken Fisher cautions is rooted in four persistent worries. Even as the market advances, fears about policy shifts, costs, data reliability, and long-term fiscal health are shaping allocations, hedging strategies, and whether the next move is up or down. Fisher, founder and executive chairman of Fisher Investments, frames these questions as a “wall of worry” that can accompany bull markets and, in some cases, help explain divergent performance across regions and asset classes.

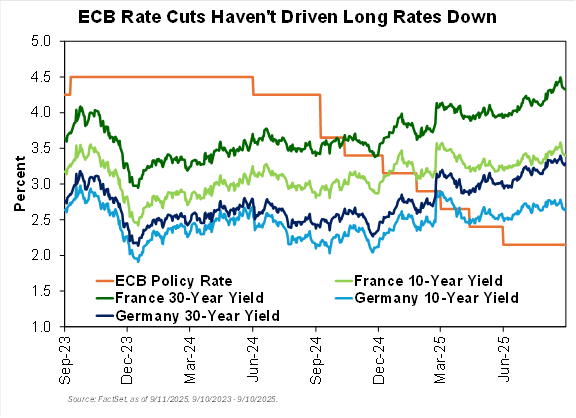

The first question centers on policy: do the economy and stock markets need a fresh round of Federal Reserve rate cuts right now? Fisher notes that cuts can steepen the yield curve—the gap between short-term and long-term rates—which historically spurs bank lending and can support equity valuations. He observes that U.S. markets this year have often lagged Europe and other regions that have priced in more aggressive easing, in part because the U.S. yield curve flipped from inverted to flat earlier this year, and lending has since accelerated. Lending rose from about 2.8% at the end of 2024 to roughly 4.5% today, suggesting the domestic economy can still fund activity without immediate relief from the Fed. While cuts could theoretically push long rates lower and jiggle mortgage rates, Fisher cautions that this outcome is not a certainty; long rates are set by global free markets and are not tightly tethered to short-rate moves. The bottom line: there is a potential but not a guaranteed path from further cuts to stronger growth, and investors should weigh the timing and scope of any easing against a still-variable global environment.

A second worry is the prospect of reshoring manufacturing—a topic that has gained attention as debates over supply chains and domestic capacity intensify. Fisher argues that a manufacturing homecoming is not inherently bullish or bearish for U.S. industrial stocks; markets care about profits, and where a product is made does not guarantee stronger margins. Reshoring can entail high upfront and ongoing costs, including stringent environmental regulations, which can compress margins if the scale of production and efficiency gains do not offset them. Furthermore, even if a shift in production were to occur, it is a long-term, complex process. Investment decisions, multi-agency permitting, and potential lawsuits can push reshoring timelines well beyond the typical 3- to 30-month horizons investors often assume. In Fisher’s view, basing current stock bets on a reshoring wave is largely speculative, given the potential for cost pressures and protracted timelines that may mute near-term performance for industrial names.

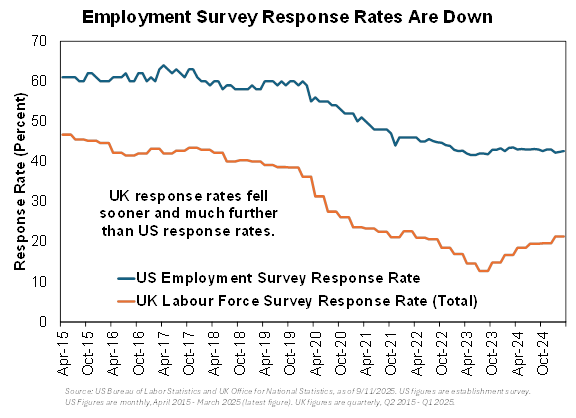

The third worry concerns the reliability of government-sourced jobs data. Fisher notes that Bureau of Labor Statistics numbers have grown trickier to interpret because firms respond less frequently to surveys and response rates are falling globally. Consequently, revisions to employment figures can be significant as more complete data trickle in, and monthly numbers can be noisy indicators that lag behind evolving conditions. While private-sector data exist for cross-checking, Fisher cautions against placing too much faith in any single data point or even a couple of months’ revisions. Jobs data, he reminds readers, are late-lagging indicators that typically confirm realities markets have already priced in, and the safest course for investors is to avoid overreacting to short-run fluctuations while watching a broader set of signals and longer-term trends.

A third image is placed mid-article to provide context on market dynamics and investor sentiment.

The fourth concern is a fiscal one: the political and financial implications of social-security funding under policy proposals such as the One Big Beautiful Bill Act. Fisher emphasizes that the Social Security Administration’s estimates under changes like a proposed $4,000 SSA tax deduction would shift the program’s insolvency date from roughly the third quarter of 2034 to the first quarter of 2034. He stresses, however, that insolvency does not equate to zero benefits or immediate bankruptcy; payroll taxes remain the primary revenue source, and even under pressure, SSA benefits could continue at a reduced level for many years. The deduction is temporary, expiring in 2028, and the overall impact on SSA revenues is relatively small—about 4% of SSA’s revenues—compared with the roughly 91% coming from payroll taxes. Politicians have strong electoral incentives to preserve Social Security, and many uncertainty factors remain, including growth, demographics, and potential policy adjustments that could alter projections.

Fisher notes that fears—whether grounded in data or political debate—serve as psychological ballast for investors, shaping both risk appetite and the search for hedges. He also argues that the environment is characterized by a mix of headwinds and policy levers that can interact in unexpected ways. The net effect, he suggests, is a market that can keep advancing even as concerns rise, precisely because the thorniest issues are not: they are long-run, structural questions that require cautious, rather than reactionary, positioning.

Another overarching point in Fisher’s framework is the need for investors to test a range of scenarios rather than cling to a single narrative. The global market system—where long-term rates are determined by a constellation of factors—from central-bank policy to inflation expectations to productivity growth—means that perfectly predicting outcomes is unlikely. The best approach, according to the column’s emphasis, is to diversify across baskets of assets, monitor both leading and lagging indicators, and avoid overconfidence in any one signal—whether it be Fed moves, reshoring timelines, or revisions to employment data.

In closing, Fisher invites readers to contribute more worries to the discussion, acknowledging that new questions will continue to surface as conditions evolve. Investors are advised to balance optimism with vigilance, recognizing that fear can coexist with opportunity when strategies are disciplined, information is checked against multiple data sources, and time horizons remain anchored in fundamentals rather than narratives. As markets press toward new highs, the onus remains on investors to weigh the dairy of cross-currents—policy, costs, data integrity, and long-term fiscal health—against the possibility that mispriced risk and structural shifts could redefine the road ahead.