Gen Z credit scores fall at fastest pace in years, driven by student debt and delinquency reporting, FICO finds

New FICO data show Gen Z's average score at 676 amid broader declines; experts urge proactive monitoring and good credit habits

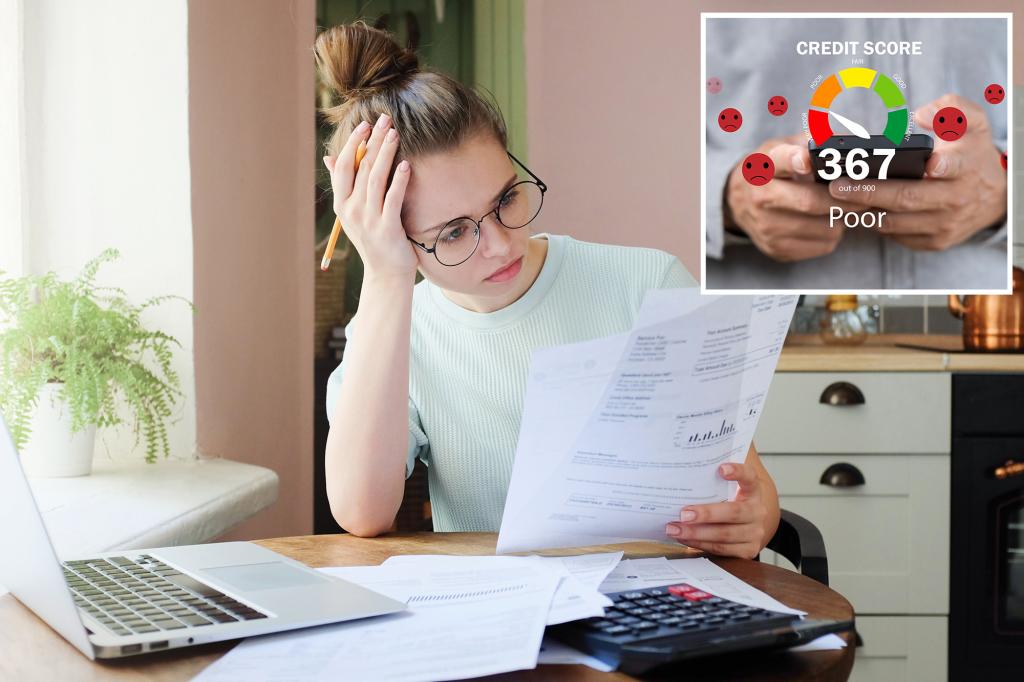

Gen Z’s credit scores dropped more than those of any other generation this year, according to a new FICO report released this week. The national average declined two points to 715, while Gen Z’s average fell three points to 676, the largest year-over-year drop for any age group since 2020.

The report notes that 34% of Gen Z consumers have open student loans, compared with 17% of the overall population. The decline in scores is linked to the resumption of delinquency reporting for federal student loans after a long pause during the pandemic. The U.S. Department of Education paused federal loan payments in March 2020; payments were scheduled to resume in 2023, but the administration extended a one-year grace period that ended in October 2024. This summer, the Trump administration restarted the collection process for outstanding student loans, with plans to seize wages and tax refunds if the loans continue to go unpaid. Roughly 5.3 million borrowers who are in default could have their wages garnished.

Beyond student debt, a weak job market and high inflation are weighing on younger households’ ability to stay current on payments. A lower credit score can complicate or raise the cost of car loans, mortgages, credit cards, auto insurance and other financial services.

“They’ve had so many different ongoing causes of economic instability that have really been with them as they’ve been growing up; those factors make it a lot harder for this generation to stay financially stable,” said Courtney Alev, consumer advocate at Credit Karma.

“Even with those challenges, younger consumers also have the most potential for score improvement,” said Tommy Lee, senior director at FICO. When it comes to score calculation, the most important factor is paying on time, accounting for about 35% of the score, he noted.

Experts offer practical steps for anyone whose score has slipped: don’t avoid checking your score, since knowing where you stand helps you plan. Use free tools from Experian, FICO and Credit Karma to verify your current number. Pay on time, whether the minimum due or the full balance, and consider setting automatic payments if juggling multiple debts. Keep credit utilization low but not zero, ideally between 10% and 30%. If you’re struggling to pay debt, avoid taking on new debt. Credit scores are dynamic and change with your financial behavior, so adopting responsible habits can drive improvement over time, said Lee.

The report underscores that Gen Z’s relatively inexperienced credit history also means more room to grow, and that with disciplined credit behavior, scores can rebound as economic conditions stabilize.