Spike in gilt yields offers investors chance to lock in tax-free returns

Surging long-term UK government borrowing costs pushed 30-year gilt yields to multi-year highs, presenting opportunities for buy-and-hold savers and higher earners using ISAs and pensions

A jump in the cost of UK government borrowing has pushed yields on long-dated gilts to levels that give ordinary investors an opportunity to secure generous, tax-efficient returns by buying gilts directly and holding them to maturity.

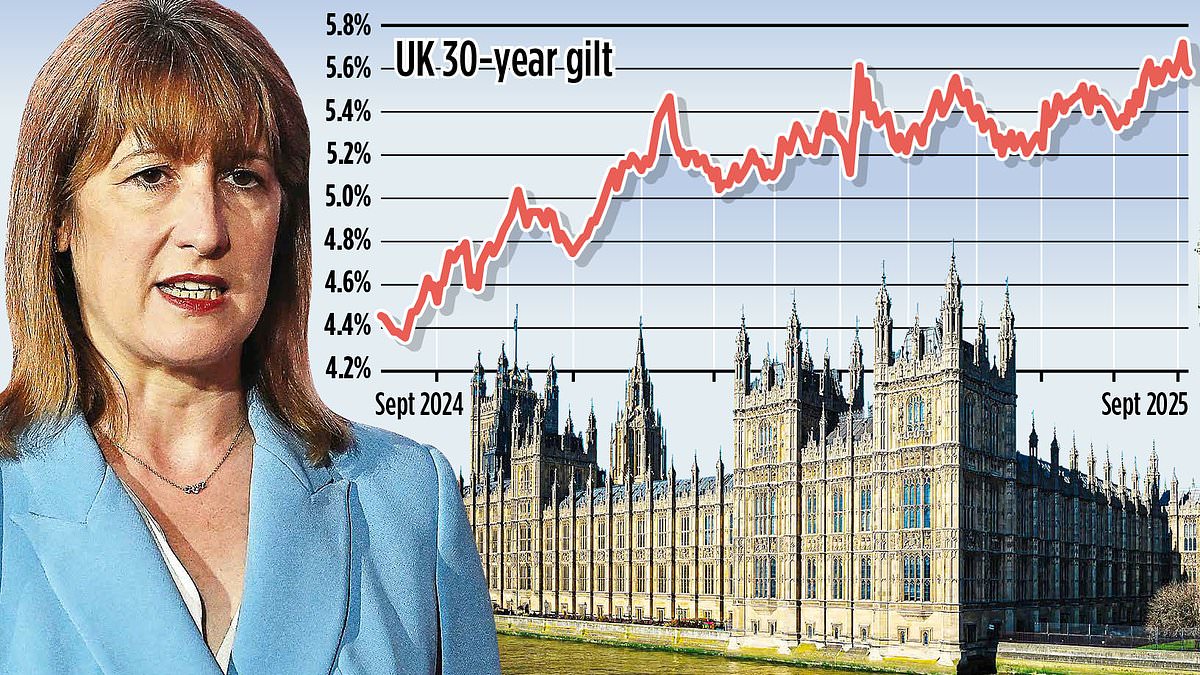

Last week the yield on 30-year gilts reached about 5.75 percent, a level not seen in years amid turbulence in bond markets. That rise means new and existing gilts now pay higher coupon rates, allowing investors who purchase and hold them to earn a fixed income above 5.5 percent for decades in some cases. Because capital gains tax is not charged on gilts, investors who buy and later sell at a profit can do so without incurring CGT liability.

Gilts are the UK government’s debt securities, issued to finance public spending such as infrastructure and services. They pay regular interest (coupons) and return the face value at maturity. Investors can buy gilts when the government issues new stock at auction or purchase previously issued gilts on the secondary market through online brokerages and DIY investment platforms. Many platforms now allow individual investors to buy single gilts and to hold them within tax-efficient wrappers such as ISAs and personal pensions.

Market participants say the recent spike reflects a combination of higher Bank of England expectations, inflation dynamics and a shift in global bond sentiment. The rapid move in yields has been unwelcome for the Treasury, which faces higher costs on new borrowing, but it has created an opening for savers who regard government debt as relatively low risk compared with corporate bonds or equities.

Buy-and-hold investors who take gilts to maturity will receive the coupon payments regardless of interim price movements, effectively locking in the yield at purchase. Alternatively, some investors who acquired gilts when yields were lower could sell while yields retreat and prices rise, crystallising a profit that, unlike gains on many other investments, is not subject to capital gains tax. Financial advisers report that higher earners in particular have been steered toward gilts for their combination of predictable income and favourable tax treatment.

DIY platforms and retail brokerages have lowered barriers to entry for individual investors, offering straightforward execution, access to different maturities and the ability to place gilts inside ISAs and pensions. That accessibility allows savers to build strategies such as laddering maturities, which staggers reinvestment risk, or selecting long-dated issues to lock in current elevated coupon rates for many years.

While gilts are generally regarded as low risk relative to corporate debt, they are not without drawbacks. Prices of existing gilts can fall if market yields rise further, creating losses for investors who need to sell before maturity. Inflation that outpaces coupon payments can erode real returns, and policy shifts that change interest-rate expectations will affect secondary-market values. Investors should also consider liquidity; very long-dated or lesser-traded issues can be harder to trade quickly at a favourable price.

The recent move in yields comes amid a difficult backdrop for the Treasury, which must fund government activity at higher rates than in recent years. That dynamic is part of broader market volatility in fixed income as central banks, economic data and geopolitical developments influence investor expectations. For savers, the rise in yields restores a return profile in government debt that was largely absent during the prolonged period of ultra-low rates.

Advisers say the key practical steps for those considering gilts are to decide an appropriate maturity profile, confirm whether to hold within an ISA or pension for extra tax efficiency, and to be clear about whether the objective is steady income to hold to maturity or shorter-term trading for price moves. Retail investors who are uncertain about matching gilts to their goals are advised to seek regulated financial advice.

As gilt markets settle, yields could move lower or higher depending on future economic data and policy decisions. For now, the spike in long-term gilt yields provides a straightforward way for some investors to secure higher, tax-efficient government-backed income, while highlighting the fiscal challenges facing the Treasury as borrowing costs rise.