Surge in gilt yields hands investors chance to lock in tax-free gains

Spike in UK borrowing costs pushes 30-year gilt yields above 5.7%, prompting retail demand to buy direct and hold in ISAs or pensions

A sharp rise in the cost of UK government borrowing has created an opportunity for investors willing to buy long-dated gilts to lock in above-market returns, industry participants say.

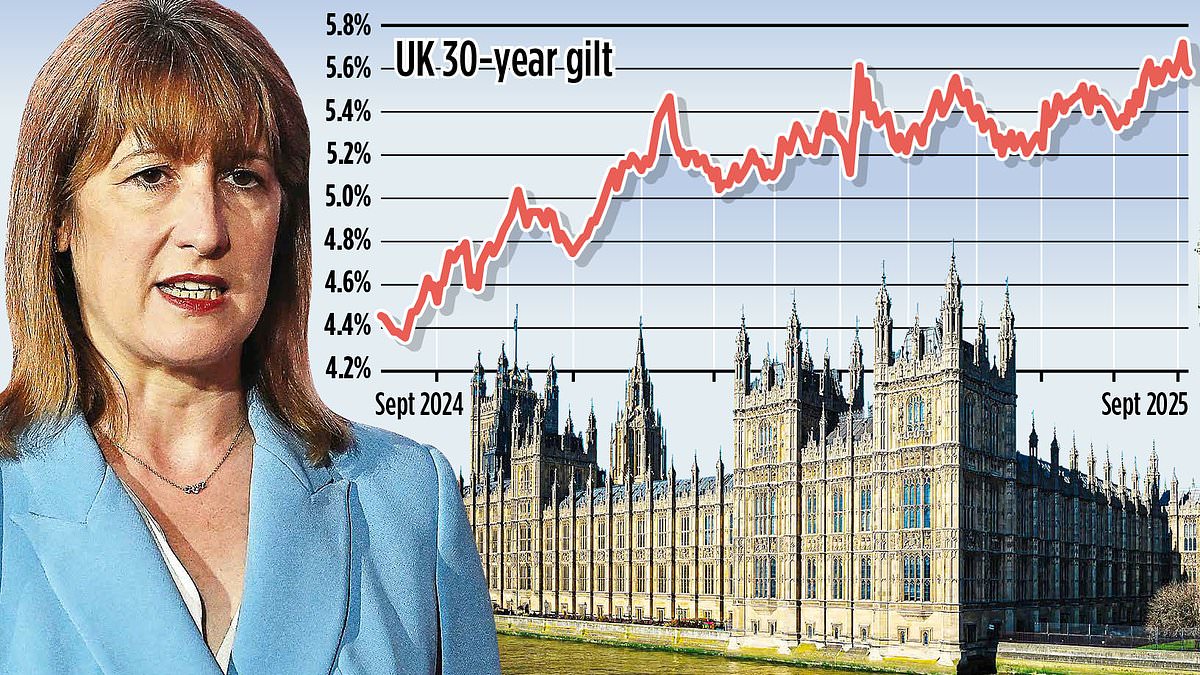

Volatility in bond markets last week saw the yield on 30-year UK government gilts climb to about 5.75 percent. That level effectively offers investors a long-term annual return in excess of 5.5 percent if they buy and hold those securities to maturity. Because capital gains tax is not levied on gilts, investors who purchase while yields are high and later sell at lower yields can realise a tax-free capital gain.

Gilts are the UK government’s debt securities issued to finance public spending and investment. Like other bonds, their prices move inversely to yields: when market interest rates rise or sentiment deteriorates the price of existing gilts falls and yields rise. Conversely, if yields later fall, the market value of previously issued gilts increases, producing a capital gain for holders who sell before maturity.

Retail access to individual gilts has expanded in recent years as do-it-yourself investment platforms and some advisers make it straightforward to buy single issues and hold them inside tax-wrapped accounts such as Individual Savings Accounts or workplace and private pensions. Holding gilts within an ISA or pension shelters interest income and any capital appreciation from the tax that otherwise applies to unwrapped investments.

The recent sell-off in government bonds came amid a broader repricing across fixed income markets and has raised the cost of servicing government debt, a development described by market commentators as unwelcome for the Treasury. Higher yields increase borrowing costs for the state on new issuances, a situation that can complicate fiscal planning for the chancellor.

Investors assessing the opportunity should weigh several factors. Buying gilts and holding to maturity eliminates market-price risk over the life of the bond, leaving the purchaser to collect the scheduled coupon payments and the return of principal at maturity. Those who buy with the intention of selling earlier are exposed to market volatility: if yields rise further before they sell, the market value of their holding can fall.

Interest rate expectations, inflation prospects and the Bank of England’s policy path are central to price moves in gilts. While the default risk on UK sovereign debt is treated as low by investors, longer-term bonds are sensitive to shifts in real yields and to global market sentiment, which can drive sharp but temporary price moves.

Financial advisers have increasingly cited gilts as a tool for higher earners seeking tax-efficient fixed income allocations, particularly when yields are elevated. Platforms that offer access to single gilt issues allow investors to target specific maturities — from short-dated to 30-year and beyond — matching cashflow needs or duration preferences.

Regulatory and tax rules also shape the attraction of gilts. Capital gains on gilt holdings are exempt from UK capital gains tax, a distinct feature compared with many other securities. Income from gilts is taxable outside tax-advantaged wrappers, so holding them in ISAs or pensions preserves both the income and any price appreciation from tax charges.

Market participants caution that opportunities linked to high gilt yields depend on future rate moves. If yields subsume recent highs and stay elevated, investors will collect higher coupons but could face further near-term price declines if markets turn. If yields retreat, holders who sell can realise tax-free gains.

For investors considering exposure, market-making conditions, liquidity in specific gilt issues and the costs of trading on retail platforms are practical considerations. The Treasury continues to issue gilts at regular auctions and on the secondary market; prospective buyers can obtain individual issues through brokers and online platforms or gain exposure via funds, though fund investors do not benefit from the capital gains exemption in the same way as holders of individual gilts.

As the gilt market absorbs the recent repricing, retail and professional investors alike will watch upcoming economic data and central bank signals for indications of whether elevated yields will persist or begin to unwind, shaping both government borrowing costs and the returns available to those lending to the state.