VAT guidance gaps for disabled drivers spotlight consumer case in car market

Money Mail column details a £3,007 VAT dispute over a modified MG3 and surveys dealer guidance, HMRC rules, and Motability developments, alongside several related consumer complaints.

A recent Money Mail column highlights a disputed VAT charge on a car bought by a disabled driver and broader guidance gaps at car dealers, HM Revenue and Customs rules, and the Motability framework.

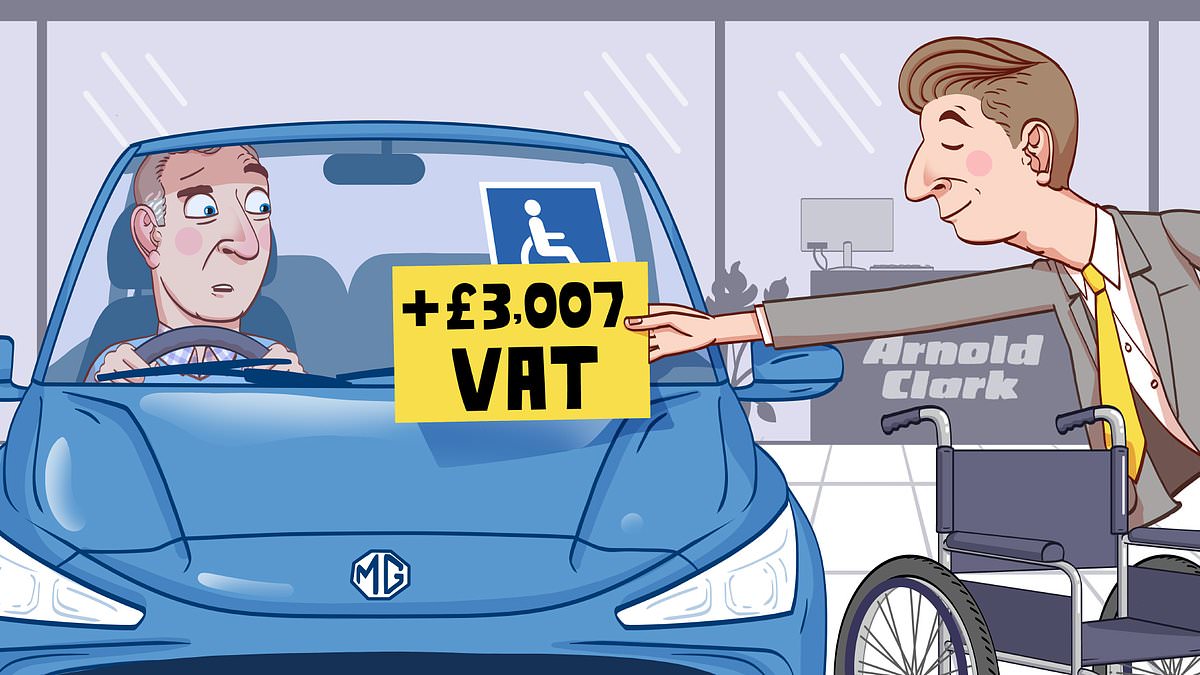

The case centers on W. R., a reader from Whitley Bay, Tyne and Wear, who says Arnold Clark Automobiles charged £3,007 in value-added tax on an £18,000 MG3 hybrid purchased from an Arnold Clark dealership in October 2024. The buyer says she is disabled following a December 2023 traffic accident that left her with life-changing injuries and mobility challenges. She and her spouse visited Arnold Clark’s Shiremoor dealership in Newcastle while she used a wheelchair and had lost a leg, and she believed the vehicle had been modified to accommodate a disability. The modifications were performed by Bewick Mobility, which indicated the work would be VAT-exempt. Soon after returning home, she learned that the VAT rule could apply to a full car purchase, but only under specific conditions. In February 2025, during a casual conversation at a rehabilitation clinic, she realized she might have qualified for the exemption and promptly requested a refund from Arnold Clark. The dealership refused, directing her to HM Revenue & Customs instead.

The dispute has drawn attention to how HMRC’s rules on VAT relief for vehicles modified for disability are applied in practice. HMRC guidance indicates that disabled drivers cannot reclaim VAT directly from HMRC; instead, eligibility is assessed by the dealer, and relief can apply when a car is designed for a wheelchair user or is substantially and permanently adapted to enable travel. The reader’s worry was that the vehicle was adapted after purchase, potentially complicating eligibility, and she argued that the showroom’s guidance—or lack thereof—might have influenced her purchasing decision.

In response to questions about the case, Arnold Clark said staff are trained to advise on entitlements for Motability customers (those seeking to lease vehicles under the Motability Scheme) but not to provide guidance on funding options outside that scheme to cash buyers. The company added that it cannot advise on specific funding options or support available outside the Motability scheme and recommended independent guidance from relevant organizations or local authorities to explore possible financial assistance. A spokesperson for Motability Operations noted that while dealers are trained to support customers who want to lease through the Motability Scheme, guidance on HMRC VAT rules for car purchases would be a matter for the dealership.

The columnist subsequently took the matter to the Motor Ombudsman in hopes of a different outcome, given the lack of clear in-showroom guidance and the charitable aim of ensuring disabled drivers receive appropriate information at the point of sale. The episode has prompted broader questions about how car dealers communicate disability-related entitlements and what recourse consumers have when confusion arises around VAT relief.

Beyond this central case, the Money Mail column includes a series of other reader notes illustrating similar friction in consumer finance and services. In Hertfordshire, executor M. F. recounts British Gas’s handling of a refund that was issued in the name of the executor’s deceased sister. The estate had been managing the property and its utilities since the sister’s death in June 2024. A cheque for £246.70 arrived on July 7, 2025, but it was made out to the deceased. After months of follow-up, British Gas transferred the funds by bank transfer to the executor and offered a goodwill gesture as acknowledgment of the inconvenience caused by delays and misdirected correspondence. The piece stresses the importance of properly closing a late customer’s account when in credit and ensuring refunds are directed to the correct party to avoid delays in winding up an estate.

Another reader, C. C., asked why Ford Money has closed a savings account containing £9,000 and why the bank is seeking information about the source of the funds and private financial details that the customer cannot provide because they do not use online banking. The note indicates Ford Money plans to return the funds to the customer’s source account, effectively closing the matter.

As part of the Money Mail roundup, readers report ongoing issues with other providers as well. A former customer of Virgin Media faced a debt-collection threat for a missing router, despite having returned the equipment five years earlier; the company apologized and removed the debt from the account. Admiral’s pet insurance arm faced a delay in issuing a £16.90 refund, with the customer receiving not only the refund but also a £100 goodwill gesture after inconsistent information and service delays. The insurer cited missed premium payments and cancellations outside the 14-day cooling-off period as reasons for the originally anticipated refund not being due, though the eventual resolution satisfied the reader.

The broader takeaway from these notes is that a convergence of consumer finance, mobility entitlements, and retailer guidance continues to shape the reliability and speed of customer redress in a complex market. The disabled-driver VAT case, in particular, underscores how important it is for dealerships to offer clear, accessible information on entitlements that may affect large purchases and ongoing service agreements.

From a business and market perspective, the episode highlights several implications:

First, dealers face increased scrutiny over how they present affordability and relief options to customers who have disability-related needs. The absence of explicit guidance on VAT relief for cash buyers, in particular, may lead to misinformed purchasing decisions and potential disputes that can culminate in external dispute resolution pathways such as the Motor Ombudsman.

Second, regulatory clarity matters. HMRC’s stance that relief is not reclaimed from tax authorities by disabled drivers but must be pursued through dealers—who assess eligibility—places emphasis on dealer diligence and internal training. The market response to these cases may push more dealers to standardize information delivery and to provide clearer pathways for customers seeking disability-related relief.

Third, the case shows how customer trust hinges on timely, accurate handling of refunds and estate-related payments. The British Gas and Ford Money notes illustrate how delays or misdirected processes can erode confidence in service providers, even when issues are ultimately resolved with goodwill gestures or refunds.

Finally, the accumulation of such consumer notes in a single Money Mail column provides a snapshot of how business-to-consumer activity intersects with public-service guidelines and regulatory oversight. It underscores the need for transparent disclosures at the point of sale and for consistent practices across departments within large retailers and financial institutions.

As the Market and Consumer Affairs beat continues to track these trends, readers will likely watch for developments: whether Arnold Clark and similar retailers adjust their sales guidance to include explicit VAT-relief pathways for disabled buyers, whether Motability and dealer partnerships refine their training and communications, and whether regulators issue further clarifications that reduce confusion at the critical moment of purchase. The outcome of the Motor Ombudsman inquiry into the disabled-driver VAT case may also set a precedent that influences how dealerships approach post-sale support and eligibility discussions in the mobility and automotive sectors.

For readers seeking clarity on their own situations, the Money Mail column continues to welcome letters and case details. Always verify eligibility with HMRC rules and consult independent guidance when in doubt about complex tax reliefs or eligibility for disability-related benefits tied to vehicle purchases.