Care home fees more than double to £7,500 a month in five years, family says

Rising staffing and operating costs, plus changes in residents' assessed needs, push private care costs higher as families exhaust savings

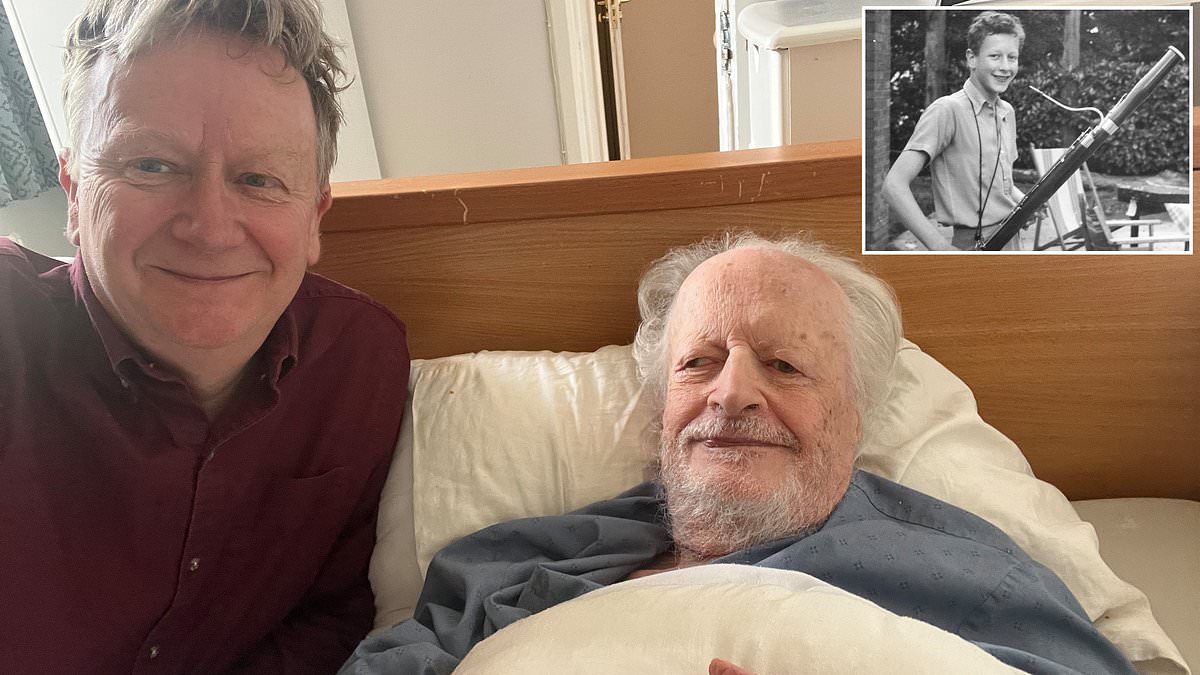

A family in West Sussex says care home fees for a man who survived a catastrophic stroke have more than doubled to £7,500 a month over five years, highlighting growing pressure on households that fund residential and nursing care privately.

The resident, identified as Richard, had lived in a Horsham care home where his monthly standing order rose from about £3,410 in 2020 to £7,500 with a review effective Jan. 1 this year. The care operator said funded nursing care—a separate NHS payment that in his case partially offset charges by roughly £700 to £800 a month—was already applied and that the increases reflected both rising care needs and higher running costs.

The home operator, DSL Care Ltd, attributed earlier increases to staff costs and Covid-19 and cited the government rise in employers' National Insurance as a factor in more recent adjustments. The provider also pointed to an "increase in the amount of care and supervision needs, mainly due to medication management and falls risk management," as justification for the latest 15% increase, according to the family.

Family members said they asked whether the resident might qualify for NHS Continuing Healthcare (CHC), which can cover care costs in full for people with primary health needs, but were told there was "not enough complex nursing care evidence to support this." The family calculates that half of the fees are covered by state and private pensions and disability payments while the remainder is paid from the man's savings.

The case is not isolated. Industry data show roughly 400,000 people live in residential and nursing care in the U.K., and only about half receive local authority or NHS financial support. Average private costs vary by type of care: industry figures cited by experts put the average monthly cost of residential care at about £5,164 and nursing care at about £6,180.

Charities and legal advisers say the pattern of rising fees is straining families. Caroline Abrahams, director at Age UK, said most care recipients must meet some or all costs themselves and are being squeezed by higher bills as local authority funding fails to keep pace. Heledd Wyn, director at the Association of Lifetime Lawyers, pointed to higher staffing costs, rising insurance premiums and the widening gap between what councils can pay and what private providers charge.

Local authority support in England is means-tested. Current rules set a capital threshold—above which people must fund their own care—at £23,250, with higher limits in Wales and Scotland. In the family's case, advisers estimated that, if fees continued at recent rates, the resident's savings would fall below the threshold within several years, potentially triggering a means test and local authority involvement.

After discussions, the family moved the resident to a lower-cost home charging about £1,500 less per month. The move, they say, has extended the period before savings are exhausted but also illustrates the disruption families face when private funding becomes unsustainable. Industry representatives warn that when local authority payments are significantly lower than private rates, residents may be asked to move unless families or the provider make up the difference.

Regulatory and complaints routes exist. The Local Government and Social Care Ombudsman recently upheld a complaint in which a provider increased charges without evidence of assessed need or appropriate contract changes; the case was referred to the Care Quality Commission, which cancelled the provider's registration. The ombudsman said providers must assess and document needs before changing contracts and charges.

Advisers recommend several steps for those planning or currently paying for care. Early financial planning and specialist advice can help families identify benefits and funding options, including Attendance Allowance and tailored financial products such as immediate needs annuities, which provide guaranteed monthly payments in exchange for a lump sum. Legal instruments such as Lasting Powers of Attorney for finances and health and welfare can speed decision-making if someone loses capacity. Families are also advised to request formal needs assessments from local authorities, pursue CHC assessments if medical needs are dominant, and seek contract reviews by solicitors experienced in later-life care to clarify which fees are fixed and which can change.

Industry groups and care providers say they are operating under cost pressures that leave few options but to pass on rises. Ian Campbell Lyle, a director at DSL Care, said increased care needs were the main factor behind price changes and that the provider regretted the family's decision to move but stood by the quality of care offered.

The family's experience underscores the risks for self-funders as care costs rise faster than general inflation. For many, the combination of longer life expectancy and rising operating costs for providers is creating harder choices about when and how to meet the bills for long-term residential and nursing care.